Cyber insurance has changed dramatically over the last few years.

Not long ago, obtaining cyber insurance was largely a matter of completing an application, paying a premium, and hoping you never had to file a claim.

Today, the process looks very different.

Cyberattacks, ransomware incidents, business email compromise, and data breaches have cost insurers billions of dollars. In response, insurance carriers have become far more selective about the organizations they are willing to insure and the security controls they expect businesses to maintain.

In many cases, cyber insurance providers no longer view cybersecurity controls as recommendations.

They view them as requirements.

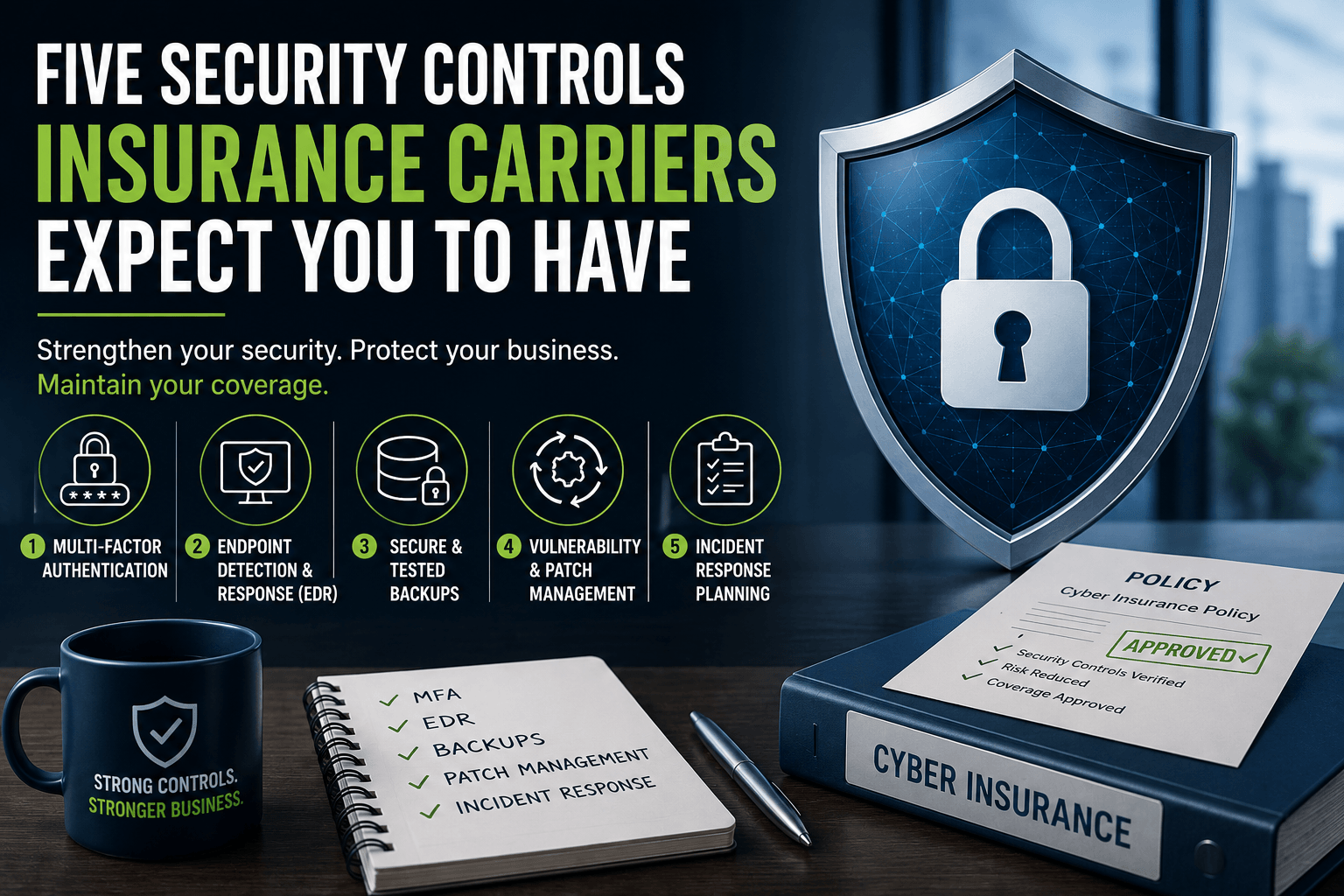

Cybersecurity Requirements

The reality is that your cybersecurity posture now directly affects whether you qualify for coverage, how much you pay, and whether a future claim will be approved.

According to Praetorian’s Cyber Insurance Requirements Guide, controls such as Multi-Factor Authentication (MFA), Endpoint Detection and Response (EDR), tested backups, and incident response planning have increasingly become baseline underwriting requirements rather than optional security enhancements.

The good news is that the same controls that help organizations qualify for cyber insurance also help reduce the likelihood and impact of a cyber incident.

1. Multi-Factor Authentication (MFA)

If there is one cybersecurity control that nearly every insurance carrier expects to see, it is Multi-Factor Authentication.

MFA requires users to provide an additional verification factor beyond a password, making it significantly more difficult for attackers to gain access using stolen credentials.

This matters because credential theft remains one of the most common attack methods used by cybercriminals.

Insurance carriers frequently require MFA on:

- Microsoft 365 accounts

- Remote access systems

- VPN connections

- Administrative accounts

- Cloud applications

- Financial systems

Many carriers will deny coverage or significantly increase premiums if MFA is not deployed consistently across critical systems. As noted in Comnexia’s Cyber Insurance Requirements Overview, MFA remains one of the most requested controls during cyber insurance underwriting and renewal reviews.

This aligns closely with the identity-first security approach promoted through Cybersecurity Services. Because today, attackers are not breaking through firewalls.

They’re logging in with compromised credentials.

2. Endpoint Detection and Response (EDR)

Traditional antivirus software is no longer enough.

Modern cyberattacks frequently use fileless malware, legitimate administrative tools, stolen credentials, and techniques designed to bypass traditional security products.

This is one reason Endpoint Detection and Response (EDR) has become one of the most common cyber insurance requirements.

Unlike traditional antivirus solutions, EDR continuously monitors endpoint activity and helps identify suspicious behavior before it becomes a larger incident.

According to Huntress’ Cyber Insurance Requirements Guide, EDR has become one of the most frequently requested controls because it helps organizations identify suspicious activity before it develops into a larger security event.

An effective EDR solution can help detect:

- Ransomware behavior

- Unauthorized privilege escalation

- Credential theft

- Lateral movement

- Suspicious user activity

- Malicious processes

This proactive approach aligns directly with the Predictive IT philosophy behind proactive Cybersecurity Services.

The goal isn’t simply responding to threats. It’s identifying them before they become business disruptions.

3. Secure and Tested Backups

Many organizations believe they are protected because they have backups.

Insurance carriers increasingly ask a more important question:

“Have those backups been tested?”

According to CISA’s Stop Ransomware Guide, organizations should maintain protected, tested backups that can support recovery after ransomware incidents and other disruptive events.

Insurers increasingly look for:

- Offsite backups

- Immutable backups

- Backup encryption

- Recovery testing

- Backup access controls

A backup that cannot be restored is not a recovery strategy. It’s a false sense of security.

This is one reason organizations increasingly invest in Business Continuity & Disaster Recovery Services.

Business continuity is no longer simply an IT concern. It is a business survival strategy.

4. Vulnerability Management and Patch Management

One of the easiest ways attackers gain access to business systems is by exploiting known vulnerabilities that organizations have not patched. Insurance carriers know this.

As a result, patch management and vulnerability management have become common components of cyber insurance questionnaires and underwriting reviews.

According to Kaseya’s Cyber Insurance Readiness Guide, insurers increasingly evaluate how organizations identify, prioritize, and remediate vulnerabilities across their environments.

Businesses should have documented processes for:

- Operating system updates

- Application updates

- Firmware updates

- Vulnerability scanning

- Remediation tracking

Attackers frequently target organizations that delay updates because they know publicly disclosed vulnerabilities are often left unaddressed for months.

Good patch management significantly reduces that exposure.

5. Incident Response Planning

Cyber insurance providers increasingly want to know what happens after a breach occurs.

- Do you have a plan?

- Who is responsible?

- How will you respond?

- How will you recover?

A documented Incident Response Plan has become one of the most common controls insurers look for because response speed often determines the ultimate cost of an incident.

The National Institute of Standards and Technology (NIST) provides detailed guidance for developing formal incident response procedures, defining responsibilities, and improving recovery outcomes through its Computer Security Incident Handling Guide (SP 800-61).

A strong incident response strategy typically includes:

- Defined response procedures

- Internal responsibilities

- Communication plans

- Recovery procedures

- Vendor contacts

- Escalation processes

Organizations that prepare before an incident typically recover faster and experience less operational disruption.

Why These Controls Matter Beyond Insurance

One of the biggest misconceptions about cyber insurance is that these controls exist solely to satisfy underwriters.

- They don’t.

- These controls help protect your business regardless of whether a claim is ever filed.

- They reduce risk.

- They improve visibility.

- These controls also strengthen resilience.

- They help prevent incidents from becoming disasters.

According to Hyperexponential’s Cyber Insurance Risk Analysis Guide, many insurers now view controls such as MFA, EDR, backup protection, and incident response planning as fundamental risk management requirements rather than optional policy enhancements.

In other words, insurers have recognized what cybersecurity professionals have been saying for years:

Proactive security is far less expensive than recovering from a cyberattack.

Do you have these cybersecurity solutions in place? If not, we can help.