Most businesses still think about cybersecurity and insurance as two separate conversations.

They’re not. Today, your cybersecurity posture directly impacts:

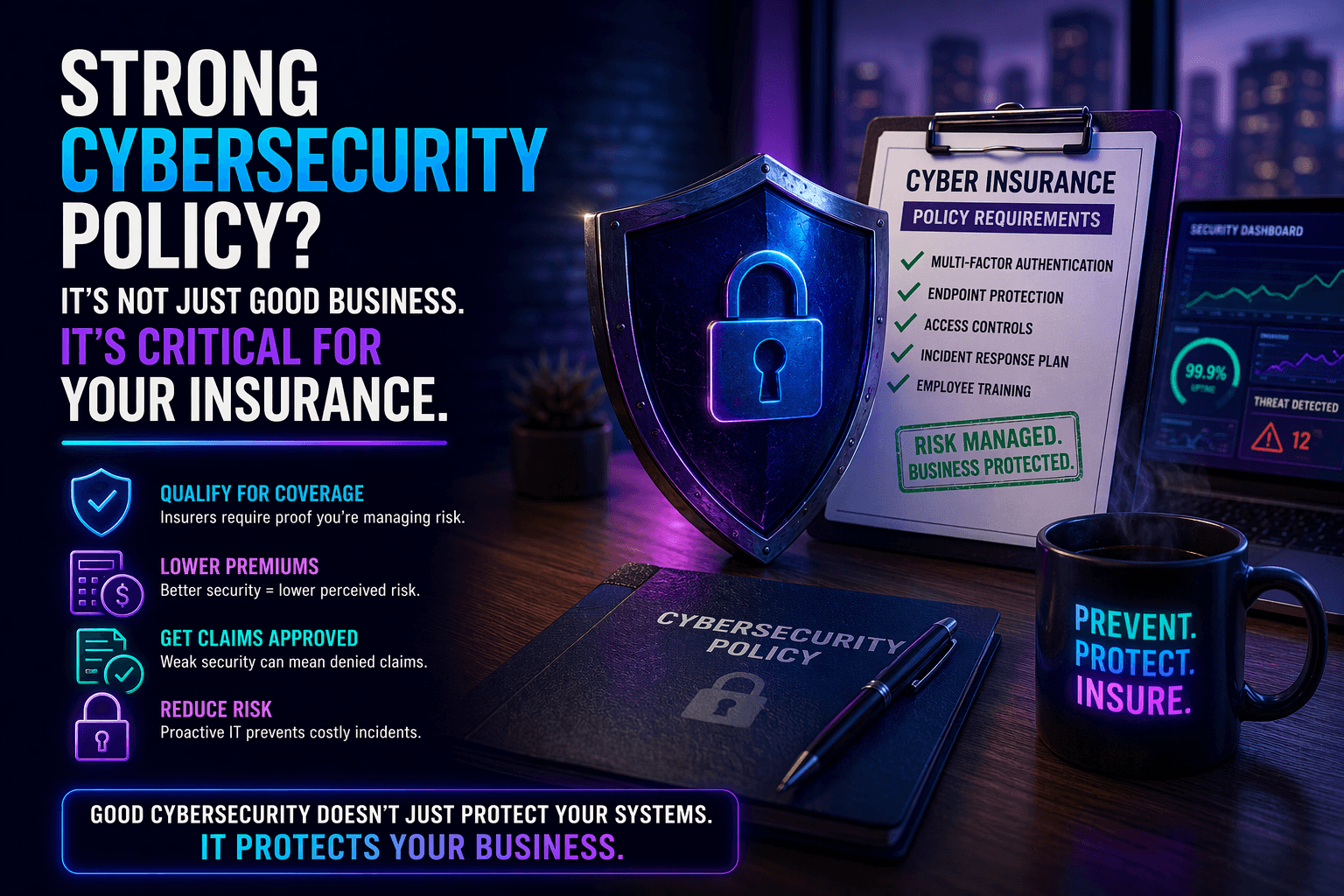

- Whether you can qualify for cyber insurance

- How much you pay in premiums

- Whether your claim actually gets approved

And increasingly, insurance carriers are asking a simple question:

Can you prove you’re managing risk, or are you just reacting to it?

Cyber Insurance Isn’t a Safety Net. It’s a Partnership

Cyber insurance is designed to help businesses recover from events such as ransomware attacks, data breaches, and system outages.

According to the Federal Trade Commission, cyber insurance helps cover:

- Financial losses from cyberattacks

- Legal costs and liability

- Business interruption

- Data recovery and remediation

Similarly, IBM explains cyber insurance functions much like traditional insurance: covering damages, lost revenue, and recovery costs after an incident.

But here’s the catch: Insurance companies are no longer willing to take on unmanaged risk.

Insurance Companies Now Require Proof of Security

In the past, you could buy cyber insurance with minimal scrutiny. That’s no longer the case.

Today, insurers require evidence of:

- Multi-factor authentication (MFA)

- Endpoint protection

- Access controls

- Incident response plans

- Employee training

For example, nearly 80% of insurers now require MFA across key systems

And requirements go further, insurers often require:

- Vulnerability assessments

- Incident response plans

- Security awareness training

This isn’t just about checking boxes. It’s about demonstrating that your business is actively reducing risk.

Don’t take our word for it, here is a statement from Cybersecurity Insurance Specialist, Gary McNall, President of GMC Insurance Brokers:

“Cyber risk is evolving rapidly, and with AI accelerating both the scale and sophistication of attacks, businesses are being tested like never before. Insurers are no longer just evaluating technology. They’re looking for clear evidence that risk is being actively managed day to day. A strong cybersecurity framework, supported by the right partners and insurance strategy, is what ultimately keeps businesses resilient and insurable.” Gary McNally, GMC Insurance Brokers, Inc.

Why a Cybersecurity Policy Matters More Than Ever

A strong cybersecurity policy isn’t just documentation. It’s proof.

Proof that:

- Systems are monitored

- Users are controlled

- Risks are understood

- Response is planned

Organizations that follow structured frameworks like the National Institute of Standards and Technology are better positioned to:

- Identify and manage cybersecurity risk

- Align with regulatory and insurance expectations

Even more importantly, organizations aligned with NIST may see reduced insurance premiums and better underwriting outcomes.

The Financial Impact: Premiums, Coverage, and Claims

This is where it becomes a business conversation.

A strong cybersecurity posture can:

Lower Your Premiums

Insurers evaluate your controls when pricing policies. Better controls = lower perceived risk.

Improve Coverage Options

Weak security can:

- Limit coverage

- Exclude ransomware

- Add stricter conditions

Increasing Likelihood of Claim Approval

If you can’t demonstrate:

- Reasonable security practices

- Policy enforcement

Your claim may be denied.

As noted in industry analysis, NIST-aligned controls are becoming a baseline expectation for securing favorable coverage.

Cybersecurity Practices That Directly Impact Insurance

Most insurance requirements map directly to core cybersecurity best practices:

Identity & Access Control

- MFA

- Least privilege access

- Identity monitoring

Endpoint & Network Security

- Endpoint detection and response (EDR)

- Network segmentation

Insurers often require documented segmentation and zero-trust principles.

Monitoring & Risk Management

- Continuous monitoring

- Vulnerability scanning

- Risk assessments

The National Institute of Standards and Technology Risk Management Framework provides a structured approach to managing cybersecurity risk across the organization

Incident Response & Recovery

- Documented response plans

- Backup and recovery strategies

Employee Awareness

- Security training

- Phishing awareness

What This Means for Small and Mid-Sized Businesses

Cybersecurity and insurance are converging. And for SMBs, that creates both risk and opportunity.

According to broader industry insights, cybersecurity is no longer a “checkbox”, it’s an ongoing operational requirement tied to insurance, compliance, and financial risk

Where Predictive IT Fits In

This is exactly where most businesses struggle. Not with tools, but with strategy and alignment.

We focus on predictive and proactive IT, meaning we focus on:

- Building proactive IT environments

- Implementing security-first architectures

- Aligning IT with business risk and insurance requirements

Cyber Insurance Used to Be About Recovery

Now it’s about proof. Proof that:

- You understand your risks

- You’ve taken steps to mitigate them

- Your business is resilient

Because in today’s environment, good cybersecurity doesn’t just protect your systems.

It protects your ability to operate, recover, and even stay insured.

Would you like to make sure your cybersecurity will save you money? Let’s chat.